Breaking News

Cost Drivers Examples In Service Industry

понедельник 04 февраля admin 94

The textbook answer defines cost drivers as those factors that determine the overall cost of operations. As an example, in manufacturing the cost drivers may be processing time or number of steps to produce the product. In service, the cost drivers could be the actual ratio of billable to non-billable time. At its core, activity-based costing (ABC) is about cost management. This means that costing in the service sector needs to be forward-looking, and ABC is a tool. There are examples of hospitals successfully implementing ABC systems in the article. Cost driver analysis in hospitals: A simultaneous equations approach.

Cost drivers are characteristics of activities or events that cause a business to incur costs. The cost at issue often is referred to as the cost object. By analyzing cost drivers, businesses can better understand the correlation between costs incurred and the activities that cause them.

Furthermore, a cost driver provides the basis for cost allocation among business units that directly benefit from the cost incurred. A cost object may appear related to different activities, but in determining cost drivers, a business must choose those that correlate mainly with the cost object, best facilitate management control and are the easiest for cost measurement. Chastushki belomorkanal torrent.

Identify the cost object. To determine cost drivers, a cost object must be first identified.

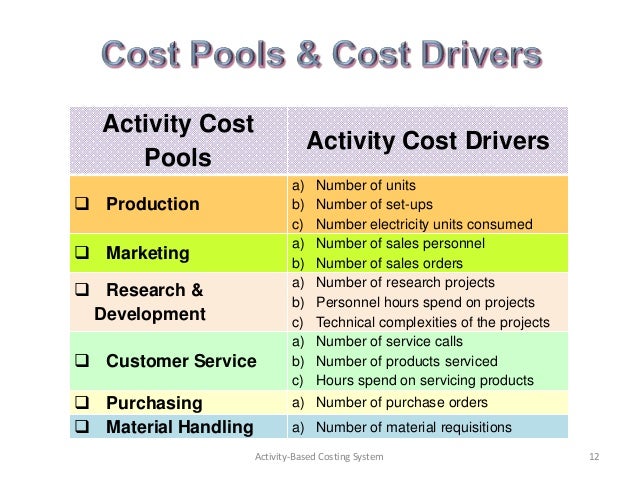

The purpose of having a cost driver is to better distribute the cost of a target cost object among its cost beneficiaries. For example, for a business that encounters regular material handling tasks, how to better allocate its total material-handling cost to different working units could be challenging. Here the material handling cost is the cost object. Having set the target cost object, the business can then determine a cost driver to help distribute the total material handling cost to different working units.

Investigate potential cost drivers. A valid cost driver must reflect the causal relationship between a specified activity and the cost incurred. Mobilemark 2007 battery test download torrent. Using the same material handling example, the working units may track their work in terms of the total number of boxes of materials handled or total weight of the materials handled. The number of boxes of materials moved and the weight of materials handled are two ways of quantifying the material-handling activities, and management may consider them as alternative cost drivers. Determining a cost driver among potential options depends on how well each cost driver may correlate with the cost object, contribute to management control and provide cost measurement. Determine cost driver correlation. In the material-handling example, management identified two potential cost drivers, suggesting that material-handling costs for each working unit be measured either by the number of boxes of materials moved or the actual weight of the materials handled by a unit.

If the materials handled are homogeneous and packed in boxes of the same size, each unit would incur an equal handling cost for every box of material handled. If the materials are different in content and packaging sizes, a unit that handles a large box of heavy material would likely incur a higher handling cost, such as requiring more labor, than a unit that handles a small box of light material. This makes it unfit to use the number of boxes handled to measure material handling cost.

In comparison, material weight as a cost driver is more closely correlated to material handling cost. Analyze the management control effect. Choosing the right cost driver may positively affect management control.

In the material-handling example, if total material handling cost was allocated to individual working units based on the number of boxes of materials moved by each unit, a unit that handles many small boxes would be assigned a higher cost than it actually incurred and a unit that handles few large boxes of materials would be assigned a lower cost than it actually incurred. This essentially would cause one unit to burden and subsidize certain cost for another unit. Consequently, the small-box unit wouldn't have a working incentive, because the more boxes it handles, the more cost it would unfairly incur -- a potential management-control problem. Using material weight as the cost driver allows equal and fair cost distribution for all units. Conclude on cost measurement. To determine cost drivers, management must also consider whether the cost measurement provided by a potential cost driver is both accurate and easy to use. While using the number of boxes to measure material handling cost is the easiest way, using it as a cost driver doesn't provide credible cost correlation, nor motivate working behaviors.